Published on

03 July 2024Reading time

4 min.

Misappropriation and loss/disappearance of static goods is not a new issue for cargo owners. The effect is widespread, not limited to any specific type of commodity and is ambivalent to the geographical location of storage, whether in the ordinary course of transit or not. The knock-on effect should not be underestimated: this type of loss also affects shippers, buyers, supply chains, warehouse keepers and collateral managers and of, course, their insurers. Substantial losses can also negatively affect local markets, disrupt trade and, dependent on circumstances, change future pricing in the locale.

To exacerbate the problem, recently these ‘events’ have resulted in larger and more complex losses, leading to higher severity of the subsequent insurance claims, as well as the resulting commercial disputes and lengthy, costly litigation.

What is this market, why do these risks exist and why are there goods in store around the globe?

The insurance market provides an invaluable facilitation service to world trade. The international trade system relies heavily on available goods being ready for manufacture, transit, storage and distribution to ensure the flow and exchange of commodities across borders. Regional distribution centres play a vital role in the efficient delivery of goods to and from local markets. Having commodities readily available allows for quick access to emerging markets and the ability to meet the demands of global manufacturing, often operating on a just-in-time model, where goods must be available precisely when needed. These goods are stored and kept in a range of storage facilities around the world, whether as bulk (piles in warehouses, silos or open yards), break-bulk (in individual bags) on racking, in containers, shore tanks or other storage methodologies and facilities.

The existence of this insurance market is closely tied to, and an enabler of, the global distribution and trading networks for these commodities. It is closely linked to trade financing (in particular, repo financing) which facilitates the buying and selling of raw materials from many industries, such as mining, farming, processing, extraction and blending. These raw commodities are often used in the manufacture of other goods, locally or regionally, so form a vital part of the supply chain for the finished goods that we use and enjoy every day. An example of this is the extraction of cobalt as a by-product of nickel / copper smelting, which is used in the manufacture of lithium-Ion batteries, found in electric vehicles and myriad other consumer products.

Types of Commodities and usage

- Coffee, tea & cocoa for drinking and as ingredients for foodstuffs.

- Sugar for food & drink

- Cotton for linen and clothing

- Gold & silver for jewellery, trading and as a store of value

- Metals: Steel, aluminium, and others

- Liquid chemicals such as acids, polymers for manufacturing plastics and some foodstuffs

- Alcohols: ethanol for pharmaceuticals and perfumes, methanol for adhesive, paint, synthetics, acrylics, naphtha for solvents and cleaning fluids

- Semi-precious metals such as nickel, cobalt used in batteries and electrical appliances, copper.

- Farming produce – Malt, wheat/corn, soya, fruit juice

- Fossil fuels: Crude oil, fuel / heating oil, gasoline, natural gas, and coal

- Pharmaceuticals: solids (tablets), liquids (medication/vaccines)

- They can be moved and stored via many methods and conveyances: in bulk (loose), break-bulk (in bales, bags, drums, or packages), or in containers or ISO tanks:

A complex network of stakeholders

The world of static commodity insurance claims involves numerous stakeholders including; commodity traders, bank financiers, buyers, sellers, local interests, international producers, farmers, wholesalers, retailers, and many others. Given the diverse range of participants, a wide range of individuals and organisations are exposed to risk of loss. As such, it is often difficult to pinpoint who is responsible for the storage and insurance of these commodities and at which points in time. This in turn can increase the challenge of identifying how and when goods have been released from stock, who the perpetrator(s) are and who is ultimately responsible for the misappropriation loss.

So, what is misappropriation?

There is no settled definition of misappropriation under English law. Misappropriation is a criminal offence and may amount to theft, or the civil tort of conversion. By the nature of international trade and to access local markets, cargo shippers/sellers/buyers must entrust their goods to third parties, for transit, safekeeping, storage and/or sale.

These third parties include:

- Shippers

- Freight forwarders

- Charterers/shipowners

- Non-vessel operating common carriers (NVOCC)

- Inland marine/trucking firms

- Collateral managers or stock management agencies

- Customs, import and export, bonded warehouses

- Warehouse keepers/other bailees for reward

- Consignment stock managers/receivers

In the absence of a settled English law definition, the Joint Cargo Misappropriation Clause (JC2017/010) defines it rather well:

Misappropriation Exclusion (Amended 15th November 2017)

"…Misappropriation [shall in this insurance be deemed to] mean the unauthorised conversion, use, release or disposal of the subject-matter insured at or from a warehouse or other place of storage whether on or offshore, other than in the ordinary course of transit, by or with the knowledge of the bailee or of any other person or entity including their officers and employees to whom the subject-matter insured has been entrusted.”

Incidents of high value static cargo disappearance, where commodities are either stolen or illegally sold are more commonplace than might be appreciated. The cargo is subsequently difficult to trace and thus, difficult to recover, either physically or financially from the potentially responsible third party(ies). This is despite the efforts of the global cargo market and their insurers to utilise more sophisticated risk management, control, security systems and technological advances, such as computerised inventories, electronic documents, and more secure product release mechanisms.

Multiple types of loss

- Use of fraudulent documents, such as bills of lading or warehouse receipts to dishonestly fabricate or exaggerate the physical existence of goods, enabling the same parcel of goods to be sold or pledged multiple times to the same or different buyers/receivers.

- Criminal gangs/organised crime exerting pressure or threats on warehouse-keepers.

- Use of falsified documents to illegally obtain release of the goods through deception.

- Swapping out high quality material for lower grade product.

- Fabricated/false break-ins, robberies, and hold-ups.

- Discovery of shortage of goods during stock taking and inspections.

- Bankruptcy or liquidation of stock or collateral managers (whether intentional or not).

- Bribery & corruption, unlawful or questionable seizures and the use of dubious court orders.

- Slow unauthorised release of goods over time.

- Co-mingling of goods with others.

- Back-door sales for cash ‘off books’.

- Unapproved product releases by collateral manager agreement (CMA)/ stock management agreement (SMA).

- Goods pledged multiple times, to multiple buyers.

- ‘Last-one out’ losses.

- Consignment stock losses*.

*a consignment stock loss is where goods have been consigned and shipped to a buyer, but risk and property in them remains with the seller/supplier. The buyer keeps them in their care and custody until required. Payment is then made, property in the goods transfers to the consignee and the product is released. This represents increased moral hazard for the consignee and higher risk for their insurers.

Price driven losses?

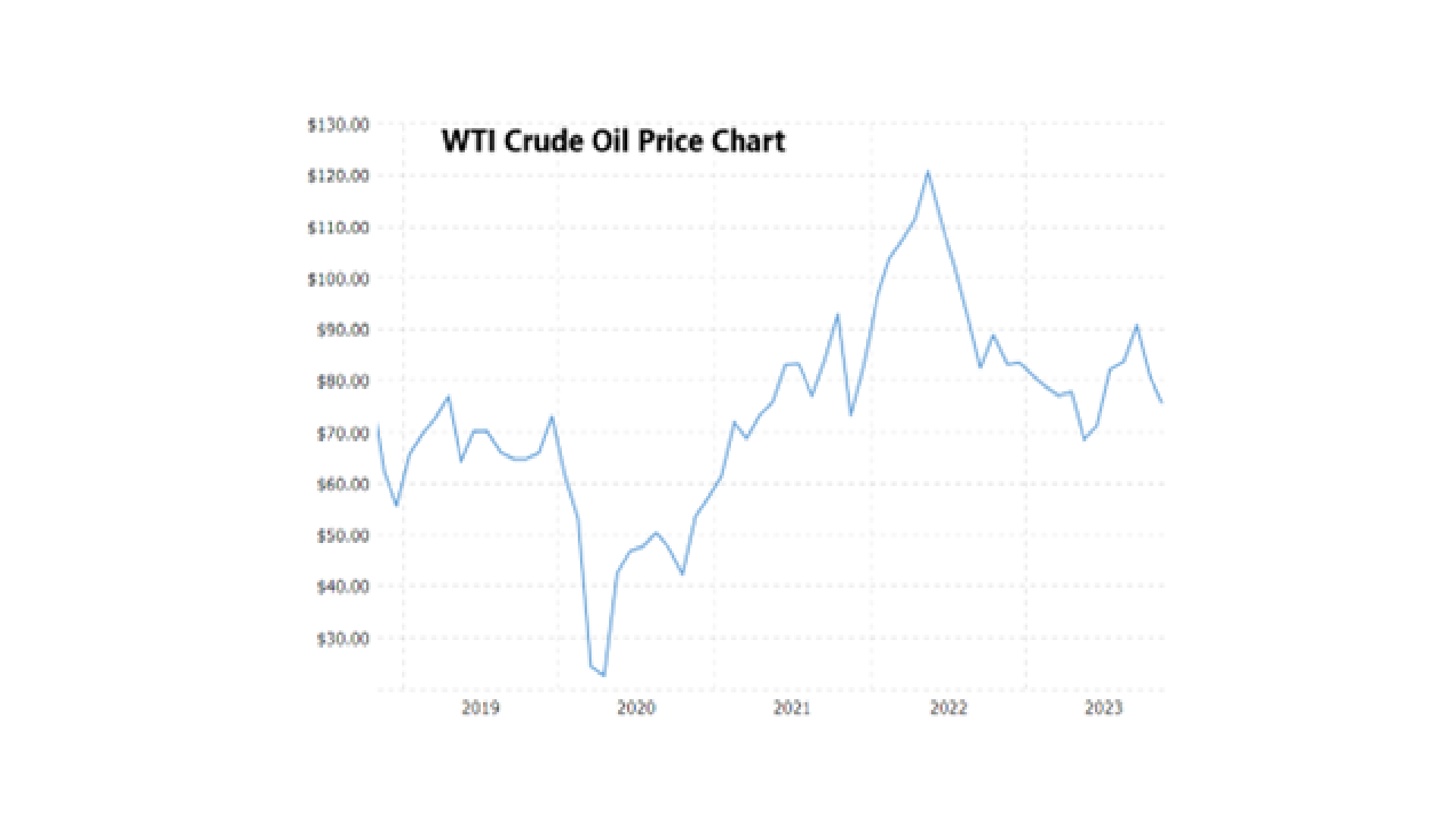

The post-Covid-19 era has brought rapid inflation and that, accompanied with supply chain issues, has resulted in hugely increased pricing of many commodities. Price increases and difficult to manage spikes in bulk commodity pricing, have caused growing issues for global traders. Take crude oil for example:

The unprecedented slump in the barrel (Bbls) cost of crude during the Covid-19 pandemic, was closely followed by a huge spike in oil pricing (to the highest level since 2008). This followed massive demand as shipping and world trade resumed and pent-up consumer spending fuelled inflation to the highest level seen in the UK since 1982.

Commodity pricing affects not only the severity of losses that may be incurred, but also changes the dynamics of supply and demand and the likelihood of loss. Here are two examples:

- If the price of a specific static commodity has rapidly decreased since entering a place of storage, the goods may be less likely to sell and may be held longer. Putting aside any deterioration or delay, goods that can’t or won’t sell create a warehouse space problem and/or a financial problem for those involved. Parties to the sale, collateral managers and storers of goods rely on the regular sale/throughput of goods for business efficacy. This financial pressure is further exaggerated if the goods are debt leveraged/trade financed. Along with trade price losses - caused by differences between the price paid and the price that can be achieved on sale – this leads to increased moral hazard for those involved to protect themselves, their business, and their profits.

- Conversely, with prices increasing, there follows opportunity for higher profit, with volumes and values at risk also rapidly increasing. This can create an insurance declaration issue, with total policy sums insured being breached. With many stock throughput policies working on a monthly or quarterly declaration in arrears basis, this can create value accumulation monitoring problems. Higher valued goods also attract more interest from criminals and are more likely to be targeted, not only by professional thieves, gangs and/or organised crime groups but by those that are involved in the safe custody/keeping of the goods under contractual agreements with cargo owners. This again leads to increased moral hazard and theft manifesting in unsanctioned product releases. These losses only become known or manifest upon stock taking, liquidation or a change in trading patterns or risk appetite, which uncovers the missing product.

Issues arising

Static commodity insurance claims revolve around addressing the theft, misappropriation, and mysterious disappearance of various commodities. Complex issues often arise. In some cases, it has been difficult to evidence whether the goods ever physically existed and whether it was even possible to (re)move the alleged quantity of goods in the given time frame. It is crucial to determine whether the insured had an insurable interest in the goods at the time of the loss, and whether the loss is an indemnifiable physical loss, a trade credit issue or a release/delivery failure, and if the latter, who is at fault. It is further complicated if there are multiple tortfeasors, and/or the alleged loss(es) occurring over an extended period and thus which insurance periods or coverages may attach, and whether losses need to be apportioned across policy years in force.

The next part of the challenge involves assessing how many losses occurred, when they occurred, and to which policy years they relate. The possibility of the same goods being sold or pledged by third parties’ multiple times, or whether there were issues of employee fidelity (with the management's tacit consent or awareness, or not) all come into question. Other issues may include classifying the loss as a mysterious disappearance if it cannot be explained, identifying whether fraudulent documents were used to gain access to premises or take delivery of goods, and evaluating the effectiveness of goods release controls and whether they were breached.

Take sugar for example. Many distributors commingle their sugar in large piles within warehouses. During inspections, they declare a specific quantity, while the actual volume may differ dramatically. Subsequently, issues emerge where, after a few months, attempts to trace the sugar reveal theft, conversion, unauthorised distribution, or clandestine shipments. There have been cases where one hundred trucks containing sugar were held hostage and threatened with violence. This complex situation highlights the intricate risks associated with the storage and distribution of commodities within the local market.

Sophisticated fraudsters use increasingly effective methodologies: recent cases involve them posing as ordinary buyers, using data and identities of a legitimate business, from internet / insider sources along with letters of credit which enabled them to collect goods multiple times and immediately sell them off to other buyers and disappearing before being found out.

Policy coverage considerations

To address these complex issues, a full, expert, and independent investigation is often necessary. But the roots of these complexities stretch far beyond the claim itself. To ensure the best protection, key policy coverage considerations must be established early on and involve thorough understanding of the terms, conditions, subjectivities, and warranties applicable to the policy and assessing the level of due diligence conducted by the insured and management's awareness. For any submitted claim, the insurer will evaluate what was disclosed about storage arrangements at the time of policy placement and examine the applicability of exclusions, such as mysterious disappearance. Additional considerations may include the presence of a fraudulent documents clause and whether it requires physical loss or damage as well as the usual compliance with the terms, clauses, conditions, and warranties of the policy.

English law cases involving misappropriation of goods:

There have been some very significant cases over the last 25-30 years which have reiterated and/or clarified how tortious misappropriation will be dealt with by the courts, what needs to be disclosed about trading relationships and patterns and how that may affect policy coverage under commodity insurance policies.

KAC Kuwait Airways v. Iraqi Airways Co (2002)

This is one of several cases regarding the Iraqi invasion of Kuwait in August 1990 and the seizure of a number of aircraft belonging to KAC. This is a leading case on the tort of conversion. It confirms that an innocent party (who has unknowingly bought goods from a thief) may still be strictly liable to the true owner in conversion. However, liability for consequential losses suffered by the true owner (loss of profit/market, business interruption, reputational damage, or other losses) is limited to those which could be expected to have been suffered as a result of that party’s conduct - the burden being on that party to establish that they were innocent. However, where someone knowingly converts another’s goods (e.g. a thief), they are acting dishonestly and will be liable on a wider basis for the actual loss suffered by the true owner. This will include any consequential losses, even if not directly flowing from the theft. The more culpable the defendant, the wider the scope of loss for which they can be fairly held responsible.

Glencore v. Alpina (2003)

This case involved the storage / blending of oil in a floating facility, which was allegedly misappropriated by the operator of the facility, and which was insured under a broad open cover. It is the leading case on what needs to be disclosed by insureds to underwriters at placement of a risk of this type, under which many commodities are insured on a stock throughput STP basis. The extent and accuracy of information given to underwriters at this stage is crucial as it may alter their view, appetite and/or pricing of the risk.

Englehart v. Lloyd’s Synd 1221 and others (2018)

This case concerned an alleged consignment of copper ingots in containers that were purchased under Fraudulent Bills of Lading, but were not in fact, ever shipped. The insured claimed an indemnity for loss of the cargo that they thought they had purchased. This case underpins the fundamental purpose of marine cargo and stock throughput insurance that the insurance covers the physical loss of or damage to goods. That is the risk with which cargo underwriters are principally concerned. If, as in Englehart, the goods never existed in the first place, there can be no physical loss or damage to them. Extensions of cover beyond the above require express words to that effect, which may rear their head in the context of misappropriation, particularly where goods may have been over-pledged to multiple parties.

Quadra Commodities SA V XL Insurance Co SE (2022)

This matter concerned what is considered a physical loss of an insured commodity, in this case, the loss of grain cargo(s) from Ukrainian warehouse(s) and a related issue as to whether an insured can have an insurable interest in an undivided bulk cargo. The insured purchased grain cargo under various contracts against the presentation by the sellers of warehouse receipts, issued by Ukrainian warehouses. The warehouse operators were fraudulently issuing multiple warehouse receipts in respect of the same goods, to multiple buyers. When physical deliveries against those warehouse receipts were sought by all buyers, there was of course not enough grain to satisfy them all.

The judgement states that an insurable interest exists where, at the time of purchase, physical goods existed in the warehouse and the insured had paid for the goods and had an immediate right to delivery. Even though the goods were misappropriated by the warehouse(s), through a fraudulent act, the loss was not caused by acceptance of a fraudulent warehouse receipt and thus not limited to the ‘physical’ language of that clause.

The case has caused some concern among insurers. There is the possibility that one parcel of goods that does physically exist at one time, is sold multiple times. The loss of that one parcel of cargo, then gives rise to multiple claims by multiple separate insureds, under multiple separate policies. In the wake of this decision, those claims may now be validly covered under all those policies, whether underwritten by the same set of insurers or not.

This case may well be under appeal to the supreme court

Conclusion

Minimising risks in static commodity insurance claims

Despite the apparent complexities, there are several processes and tools in place to assess and mitigate risk, control losses, and thus protect the insured, their brand, loss record and their underwriters. From the outset, commodity risks need to be assessed and monitored carefully. When presenting a new risk, the entire risk management framework of the Insured should be considered. Prudent underwriters will wish to understand how the insured conducts thorough due diligence when considering new locations and trading partners/markets and ensuring robust controls are in place at storage locations. Brokers can often add value to this process in guiding their Insured through the process and providing valuable in-house risk management products and experience.

Additionally, use of inspection companies or surveyors employed by insureds and their underwriters to verify the existence and volume/conformity of goods on a regular basis and conducting background checks on individuals and firms responsible for managing their collateral can help spot such issues arising early before they become very large claims. Collaboration among underwriters, brokers, and clients is essential to reduce the risk of misappropriation loss: the implementation of volume and value review regimes, along with accumulation risk exposure can assist in better understanding the risk and dynamics at play. Analysis of the prior loss history/patterns and trends concerning commodities, locations, partners, and insureds, and utilising standard market clauses that provide clarity and certainty is also advisable. The use of a carrier’s own in-house risk engineering expertise can also help to identify, assess, and minimise risk, working in conjunction with the Insured’s own risk management team.

To further improve the handling of static commodity insurance claims, meetings with clients pre-claim to establish claims relationships before a loss can be beneficial, as well as wordings reviews. Learning from prior major misappropriation incidents and avoiding pitfalls, enhancing the claims feedback loop to provide insights to underwriters, brokers, and clients, and offering advice on the risk management framework in place are additional steps that can be taken to refine and optimise the handling of these insurance claims.

These measures can collectively contribute to minimising the risk and impact of misappropriation losses and in managing the diverse complexities of global commodity trading and the related insurance claims.

Preparation is key

Static commodity insurance claims are costly for insureds and traders, complex for insurers, damaging for supply chains and potentially restricting for the growth of global trade. One cannot legislate against the unscrupulous criminal. However, through review, preparation and advice at risk analysis stage and the careful investigation, consideration, and handling of a claim in partnership with the insured and their brokers, it is a problem that can be heavily mitigated, if not completely solved.

For insurers, having widely experienced underwriting and claims team expertise with the support of experienced brokers, is invaluable to the assessment and management of risk and the control of claims, to the best outcome for all parties to the adventure.

Authors

Robert Hawes